NEWS Release - Speech- Governor Jerome H. Powell - At the The Economic Club of Indiana, Indianapolis, Indiana - November 29, 2016

Thank you for the opportunity to speak here today. My plan is to discuss the U.S. economy from three different perspectives. I will start by taking stock of the current expansion--a business cycle point of view. Then I will shift the focus to some of the longer-term challenges we face in coming years. I will conclude with a discussion of monetary policy. As always, the views I express here today are mine alone.

The Current State of the Economy

As you know, the Congress has tasked the Federal Reserve with achieving stable prices and maximum employment--the dual mandate. Today, we are not far from achieving those goals.

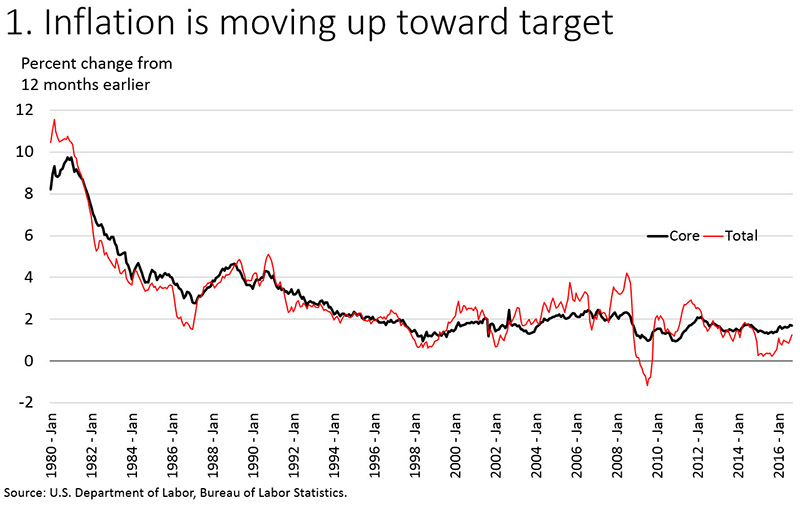

The Federal Open Market Committee (FOMC) has an objective of 2 percent for inflation, as measured by the annual change in the price index for personal consumption expenditures. The Committee sees this objective as symmetrical, so that minor deviations above or below 2 percent are treated alike.1 Inflation has consistently run below 2 percent since 2011, and is now at 1.2 percent over the past 12 months (figure 1). This headline measure of inflation has recently been held down by falling energy and food prices. We also monitor core inflation, which excludes the volatile energy and food components because they often send a misleading signal about underlying inflation pressures. Core inflation is running at 1.7 percent over the past 12 months. Both measures have gradually moved upward toward 2 percent.

{kind=link}

U.S. inflation trended steadily lower after the Volcker disinflation of 1981 to 1982 and has been low and reasonably stable for many years. In fact, for the past several years inflation has run below policy targets in many parts of the world, including here in the United States. Many of us are old enough to remember when the only challenge was to keep inflation low. But too-low inflation can also be a serious problem. Below-target inflation increases the real value of debts owed by households and businesses and reduces the ability of central banks to respond to downturns.

The public's expectations about inflation are thought to be an important driver of actual inflation. Many measures of U.S. inflation expectations--both from surveys and from market-based readings--are still well below their pre-crisis levels, although some have moved up as of late. The only way to ensure that inflation expectations remain safely anchored near the FOMC's target is to keep inflation close to that target on a consistent basis. So, while the current shortfall may seem small, it is important that inflation continue to move up to 2 percent, as I expect it will.

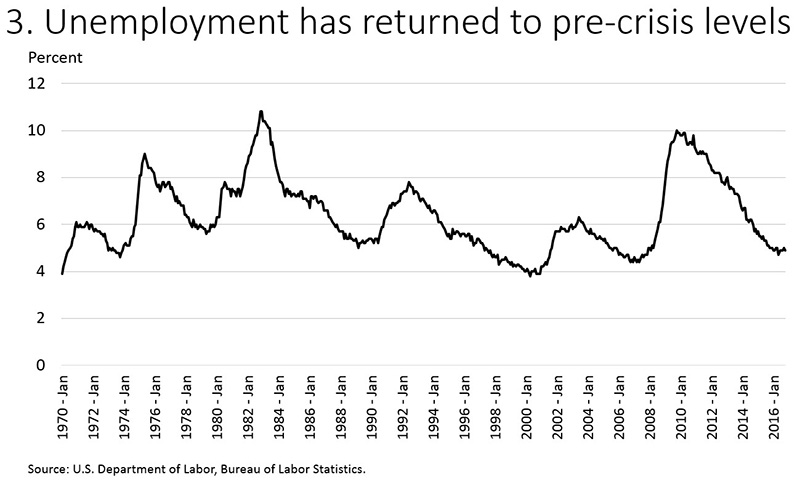

The FOMC does not have a numerical goal for maximum employment because the long-run sustainable level of employment changes over time and is determined mainly by nonmonetary factors that are outside the Fed's control, such as evolving labor market practices, demographics, social change, and fiscal and regulatory policies. Nonetheless, four times each year FOMC participants write down their estimates of the longer-run normal level of the unemployment rate (the natural rate); at the September FOMC meeting the median estimate was 4.8 percent, very close to the current unemployment rate of 4.9 percent.

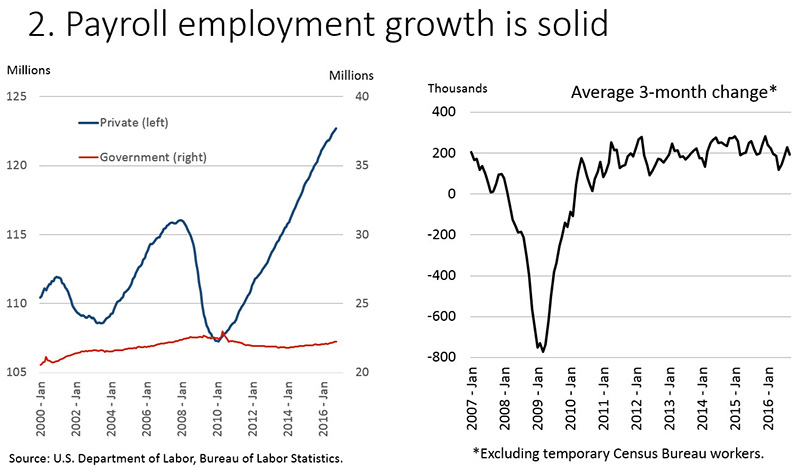

Other labor market measures are also healthy, including payroll job creation and labor force participation. Employers have been adding roughly 180,000 jobs per month so far this year--a pace a little below that of the past several years but significantly higher than underlying growth in the labor force (figure 2). Despite these strong job gains, the unemployment rate has flattened out this year after several years of sharp declines, thanks to welcome developments in labor force participation (figure 3).

{kind=link}

{kind=link}

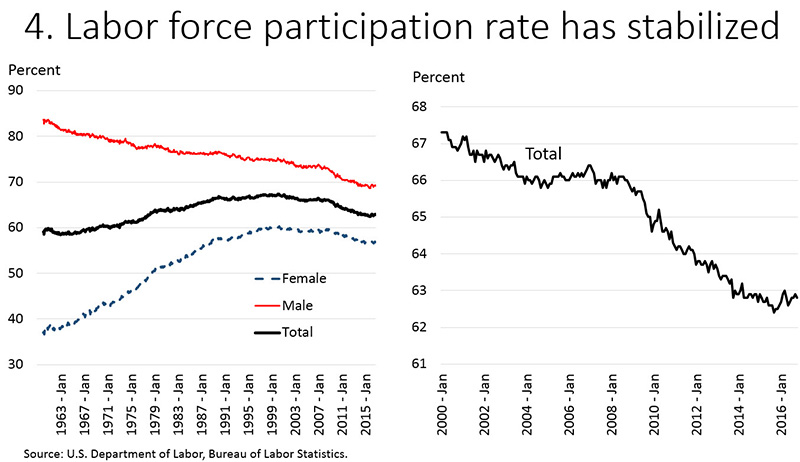

The labor force participation rate represents the percentage of adults aged 16 and over who are in the labor force, which is defined to include only those who are employed or actively looking for work. When people enter or reenter the labor force and begin to search for a job, that is generally a good thing even though at the margin their entry tends to increase the unemployment rate (or prevent it from declining). Beginning in the 1960s, labor force participation rose steadily as women entered the paid workforce (figure 4). That trend ran its course as participation peaked around 2000 and has declined steadily since then as a result of the aging of our population and other longer-run trends, notably the decline in participation by men in the heart of their working-age years. Going forward, many analysts expect labor force participation to decline at a trend rate of roughly 0.3 percent per year as a result of these factors.

{kind=link}

However, participation fell much more sharply than that after the financial crisis. Some of those who left the labor force went back to school, but others moved onto disability, took early retirement, or just became discouraged and stopped seeking work. The sharp drop raised fears that the crisis might leave behind permanent damage to our labor force. Fortunately, since late 2013, the participation rate has remained about flat and thus has gradually moved back close to its estimated longer-term trend.2 On net, people have been entering and remaining in the labor market as job prospects have brightened, offsetting the natural decline from population aging.

Surveys of households and firms also suggest that we are near full employment (figure 5). For example, respondents are now more likely to say that jobs are plentiful than that they are hard to get--a response that has generally been seen when the economy is near full employment. Job vacancies are running at high levels, and firms report that it is getting harder to find employees to fill open positions. Moreover, wages are now rising faster than inflation, and faster than output per hour. Taken together, labor market indicators show an economy that is on solid footing and close to our mandate of maximum employment.

{kind=link}

It is interesting to compare this expansion to past U.S. expansions, and also to recoveries of other countries since the end of the Global Financial Crisis. The picture is a mixed one. The current recovery has been under way since June 2009--nearly seven and a half years. It will soon be the third longest of the 20 recoveries since the founding of the Federal Reserve in 1913. GDP, or output, is now 11 percent higher than its pre-crisis peak. Employment is now 6.5 million higher than its pre-crisis peak.

Copyright: Board of Governors of the Federal Reserve System

20th Street and Constitution Avenue N.W.

Washington, D.C. 20551

page source https://www.federalreserve.gov/