NEWS Release - Vice Chairman Stanley Fischer - At "Do We Have a Liquidity Problem Post-Crisis?", a conference sponsored by the Initiative on Business and Public Policy at the Brookings Institution, Washington, D.C. - November 15, 2016

Market liquidity is the ability to rapidly execute sizable securities transactions at a low cost and with a limited price impact.1 The high degree of liquidity in U.S. capital markets historically has contributed to the efficient allocation of capital through lower costs and a mix of bank- and market-based finance that supports the flexibility of these markets.2

Regulatory changes may have altered financial institutions' incentive to provide liquidity, raising concerns brought into sharp relief by several "flash events" over the past few years. At the same time, any changes in observed liquidity are also likely accompanied by other related changes--such as in technology--and a more complete assessment of these shifts is important when we think about the effects on liquidity of changes in financial regulations that were induced by the global financial crisis.3

This afternoon, I will first review some of the concerns raised by market participants and others about market liquidity as well as highlight the challenges associated with finding clear evidence that substantiates these concerns. I will then discuss whether potential impairment of liquidity might exacerbate problems related to fire sales and leverage. Finally, I will make the case that any changes in market liquidity resulting from regulatory changes should be analyzed in the broader context of the overall safety of the financial system. This perspective naturally emphasizes potential tradeoffs between the possibly adverse effect regulations may have on market liquidity and their positive effect on the stability of the financial system.

Market Participants' Concerns

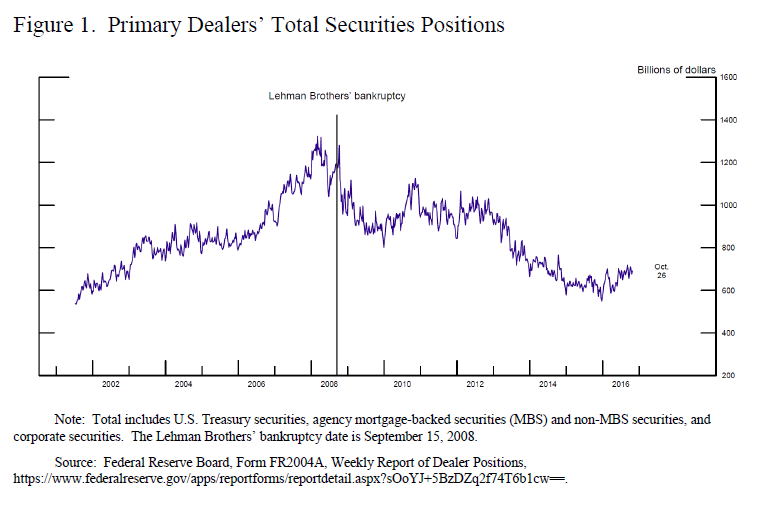

1. Decline in dealers' inventory

Market participants have cited a decline in dealers' inventories as a possible source of decreased liquidity. Figure 1 shows that primary dealers' inventories of fixed-income securities, which are predominantly used for market making, declined sharply after the Lehman Brothers failure, from about $1.3 trillion to about $800 billion, and have since fallen further to about $700 billion. The recent decline might be due in part to regulations, such as the Volcker rule and the Supplementary Leverage Ratio, aimed at making the financial system safer and sounder, as well as to changes firms may have made on their own, perhaps in reaction to the experience of the financial crisis.

{kind=link}

Regardless of the causes of the change, market participants have expressed a concern that the decline in inventories reflects in part a reduced willingness or capacity of the primary dealers to make markets--which may in turn lead to lower liquidity. However, whether markets are in fact less liquid depends on both the degree to which the decrease in primary dealers' inventories affects their willingness to provide liquidity and the extent to which nonbank firms such as hedge funds and insurance companies fill any lost market-making capacity.4

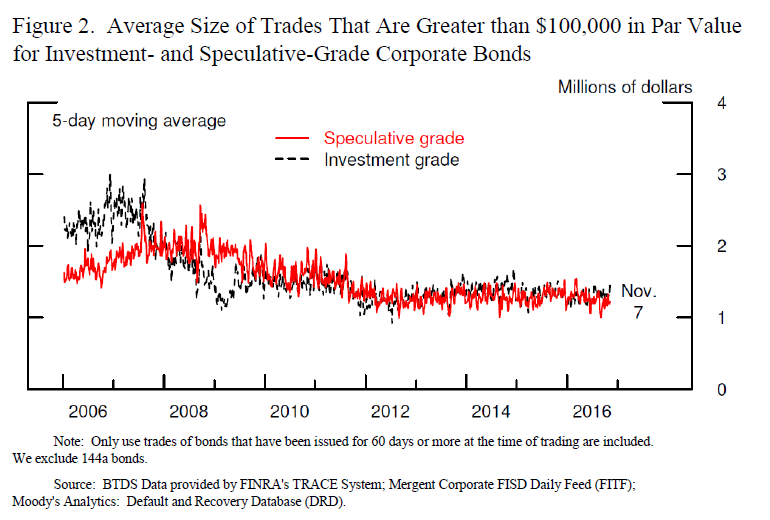

2. Decline in trade size and turnover

Market participants also often cite the decline in average trade size and turnover--the volume of trades relative to the total amount of bonds outstanding--as evidence of reduced liquidity. Figure 2 shows that average trade size in the corporate bond market has indeed declined since 2006 but has been relatively stable in the past four years. Nevertheless, this decrease may reflect a number of factors, including changes in technology or the types and preferences of institutions engaged in trades, so it may not indicate a reduction in market liquidity. Certainly, the length of this trend, roughly a decade, seems on its face more consistent with a secular trend such as technological change. Turnover in the corporate bond market has declined as well, though this evidence is also not a definitive sign of reduced market liquidity. The decline in turnover is not driven by a reduction in trading volume, but it is the result of a robust growth of the denominator, debt outstanding.

{kind=link}

3. Liquidity during times of stress

Market participants further express concern about the potential for market liquidity to become less resilient during times of stress, when it is needed the most. However, evidence on this front is difficult to gather. Some argue that market liquidity is resilient because financial markets appear to have functioned fairly well during recent episodes of high market volatility, such as following the Brexit vote or earlier this year, when oil prices were low and stock market volatility was high. Others argue that it is not. According to a recent study, the cost of trading distressed corporate bonds appears to be higher now than in the recent past.5 Specifically, the authors find that, before the crisis, the cost of a $1 million bond transaction increased about 0.7 percent following a downgrade, but--after the Volcker rule--the cost following a downgrade rose 2.4 percent. This analysis, however, is limited to episodes of distressed borrowers rather than a systemwide stress.

4. Flash events

In addition, recent flash events--such as the sharp movement in Treasury prices on October 15, 2014; the rapid rise and decline of the euro-dollar exchange rate on March 18, 2015; 6 and the swing in sterling on October 7, 2016--have led some to assert that market liquidity has become less resilient. Researchers at the Federal Reserve Bank of New York have argued that spikes in volatility and sudden declines in liquidity have become more frequent in both Treasury and equity markets.7

The Commodity Futures Trading Commission also points out that flash events are more common now.8 Market participants suggest that the rapid growth in high-frequency trading in equity, foreign exchange, and U.S. Treasury markets, along with broader concerns about less resilient liquidity, potentially explains these flash events. Nevertheless, a report on the October 15, 2014 event by the staff of the Treasury Department, Federal Reserve, and market regulatory agencies found no single factor that caused the sharp swing in prices.9

20th Street and Constitution Avenue N.W.

Washington, D.C. 20551

page source https://www.federalreserve.gov/