NEWS Release - Speech by Vice Chairman Stanley Fischer - At the Warwick Economics Summit, Coventry, United Kingdom -February 11, 2017

"I'd Rather Have Bob Solow Than an Econometric Model, But ..."

Introduction: Econometric Models and a Eureka Moment

Eureka moments are rare in all fields, not least in economics.1 One such moment came to me when I was an undergraduate at the London School of Economics in the 1960s. I was talking to a friend who was telling me about econometric models. He explained that it would soon be possible to build a mathematical model that would accurately predict the future course of the economy. It was but a step from there to realize that the problems of policymaking would soon be over. All it would take was a bit of algebra to solve for the policies that would produce the desired values of the target variables.

It was a wonderful prospect, and it remains a wonderful idea. But it has not yet happened. I want to talk about why not and about some of the consequences for policymaking.

How the Fed Makes Monetary Policy

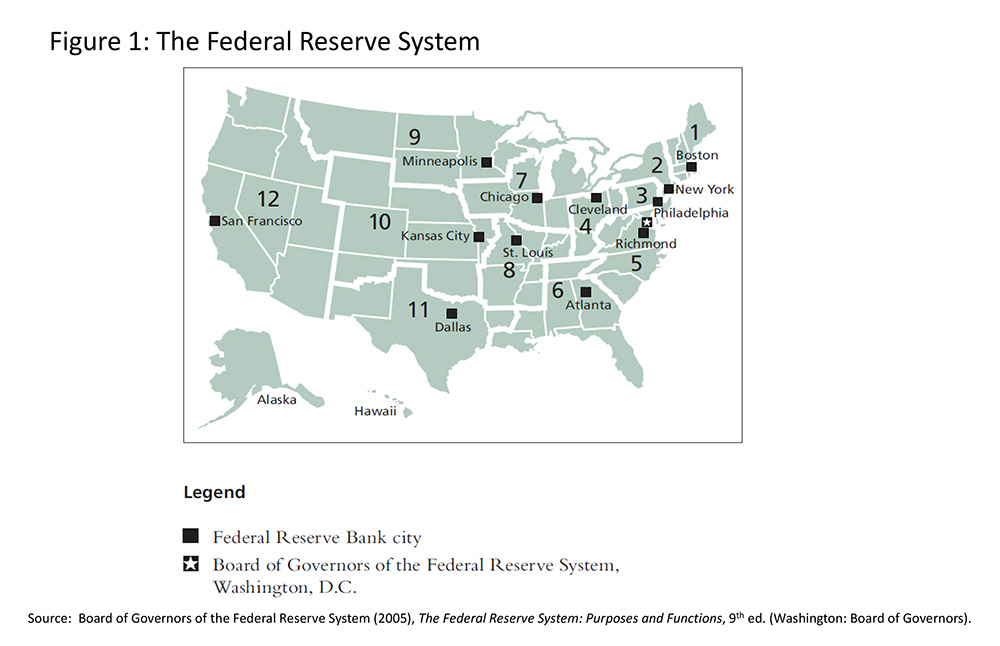

Let me begin with how we make monetary policy at the Fed. The Federal Reserve System has both centralized and regional characteristics. The System comprises the Board of Governors, located in Washington, D.C., and 12 regional Reserve Banks in cities across the United States (figure 1). The members of the Board of Governors are appointed by the President, subject to confirmation by the U.S. Senate. In contrast, the president of each Reserve Bank is selected by that Reserve Bank's board of directors, subject to the approval of the Board of Governors. This scheme was designed both to insulate the Federal Reserve from day-to-day political pressures and to ensure that all parts of the country have a voice in the central bank.

{kind=link}

Our monetary policy committee--the Federal Open Market Committee (FOMC)--meets eight times a year at the Federal Reserve Board in Washington to make decisions about whether to change the short-term policy rate and other aspects of monetary policy.2Sitting around the massive conference table will be the policymakers of the Fed--the members of the Board of Governors and the 12 Reserve Bank presidents. The Board has a maximum of seven members, but at present, two slots are empty. All of the Federal Reserve Bank presidents take part in the discussion, although only five of them have the vote at any one time.3

Each Board member or Reserve Bank president has his or her own way of preparing for those meetings. In the case of the Reserve Bank presidents, these preparations can include consultations with their boards of directors, business contacts in their Districts, market experts, and other sources. Written materials are distributed to all FOMC participants in advance of the meeting.4 The most extensive of these materials is called the Tealbook, a two-part document prepared by the Board's staff and distributed to Board members and Reserve Bank presidents.5

The first part of the Tealbook contains a summary and analysis of recent economic and financial developments in the United States and foreign economies, the Board staff's economic forecast, and dozens of tables and figures. The Board staff's baseline forecast of the most likely path for the economy over the next several years is a judgmental one, built by staff economists using their expertise on particular sectors together with econometric models and other inputs.

In addition to this baseline judgmental forecast, the staff provides model-based simulations of a number of alternative scenarios or risks--for instance, if the price of oil were to be lower, the U.S. dollar stronger, or wage growth higher than envisioned in the baseline projection. These scenarios are generated using one or more of the Board's macroeconomic models. The Tealbook also includes computations of policy paths derived from a range of policy rules and model-based estimates of optimal policy. That is to say, before our FOMC meetings, we examine analyses and forecasts produced by our staff as well as empirical results from a range of models--and, of course, material that each participant in the FOMC has gathered from his or her own research and experience.

The second part of the Tealbook includes the specific policy options that we consider at the meeting. Typically, there are three policy alternatives--A, B, and C--ranging from dovish to hawkish, with a centrist one in between. This part of the Tealbook includes an analysis of each alternative and a draft of the associated public statement that the FOMC would release after the conclusion of its meeting.

Four times a year, before the March, June, September, and December FOMC meetings, Board members and Reserve Bank presidents submit their own projections for real gross domestic product (GDP) growth, the unemployment rate, inflation, and the Committee's policy rate target, the federal funds rate. These forecasts are released to the public shortly after the FOMC meeting in the Summary of Economic Projections (SEP), and they receive a good deal of scrutiny by financial market participants and journalists.6

One important but underappreciated aspect of the SEP is that its projections are based on each individual's assessment of appropriate monetary policy. Each FOMC participant writes down what he or she regards as the appropriate path for policy. They do not write down what they expect the Committee to do.7 Yet the public often misinterprets the interest rate paths we write down as a projection of the Committee's policy path or a commitment to a particular path.

20th Street and Constitution Avenue N.W.

Washington, D.C. 20551

page source https://www.federalreserve.gov/