Governor Jerome H. Powell - At the Peterson Institute for International Economics, Washington, D.C.

Board of Governors of the Federal Reserve System

20th Street and Constitution Avenue N.W.

Washington, D.C. 20551

Recent Economic Developments, the Productive Potential of the Economy, and Monetary Policy

Thank you for the opportunity to speak here today. I will begin by reviewing recent economic developments and then turn to supply-side considerations, such as the level of potential output and the potential growth of our economy. I will conclude with a discussion of monetary policy. As always, the views I express here today are mine alone.

Recent Developments and the State of the Economy

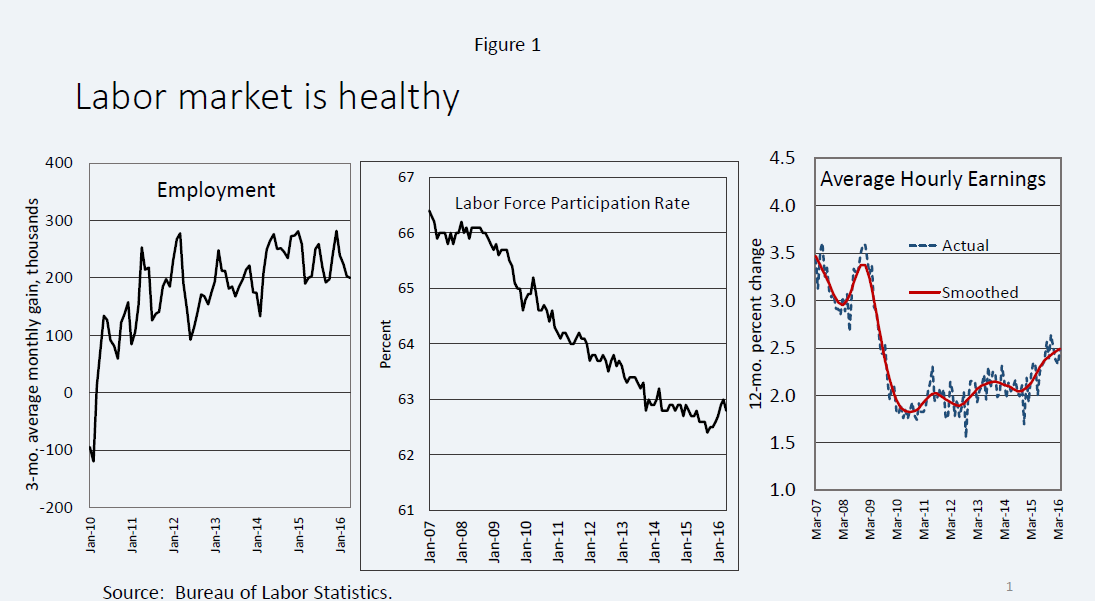

The U.S. economy has improved steadily since the recovery began seven years ago. Our economy is now 10 percent larger than at its previous peak in 2007. Employment has surpassed its 2008 peak by 5 million workers, and the unemployment rate has fallen from 10 percent to 5 percent, close to the level that many observers associate with full employment.

Labor market developments remain healthy, with employers adding roughly 200,000 jobs per month so far this year--a pace similar to that of the past several years (figure 1). Job growth continues to be substantially faster than the underlying growth of the labor force, so the labor market continues to tighten. Despite the strong job gains, the unemployment rate has flattened out at 5 percent over the past six months thanks to a welcome increase in the labor force participation rate. Meanwhile, there are tentative and encouraging signs of a firming in wages, seen most clearly in the data on average hourly earnings, which are rising faster than inflation and productivity. All told, labor market indicators show an economy on solid footing.

{kind=link}

Recent spending data have been less positive than the labor market data. Growth of personal consumption slowed noticeably in the first quarter. Business fixed investment has fallen for two consecutive quarters, mainly because of a steep decline in energy-related capital expenditures. As a result, gross domestic product (GDP) growth over the two quarters ending in March 2016 is estimated to have averaged only 1 percent on an annualized basis. This estimate may continue to move around as more data come in.1And there are good reasons to think that underlying growth is stronger than these recent readings suggest. Labor market data generally provide a better real-time signal of the underlying pace of economic activity.2 In addition, retail sales surged in April, as did consumer confidence in May, suggesting that the pause in consumption may have been transitory. Moreover, stronger demand would be more consistent with an environment that remains quite supportive of growth, with low interest rates, low gasoline prices, solid real income gains, a high ratio of household wealth to income, healthy levels of business and household confidence, and continuing strong job creation. Indeed, current forecasts for second-quarter GDP growth are for a rebound to around 2-1/4 percent.3

20th Street and Constitution Avenue N.W.

Washington, D.C. 20551

page source http://www.federalreserve.gov/