Publication - Portugal : 2016 Article IV Consultation-Press Release; Staff Report; and Statement by the Executive Director for Portugal

EXECUTIVE SUMMARY

Portugal has achieved a major economic turnaround since the onset of the sovereign debt crisis.

Access to financing was restored following the large fiscal adjustment, the external current account position has moved from a large deficit into surpluses, while the unemployment rate—though still at high levels—declined sharply.

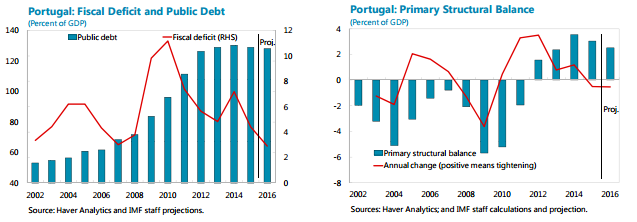

The fiscal targets for 2016 and 2017 are appropriately ambitious, but achieving them will require tackling significant implementation challenges.

More recently, however, the economic recovery in Portugal has been losing momentum.

The slowdown in economic activity that began in the second half of 2015 has persisted, despite still-favorable cyclical tailwinds and accommodative fiscal and monetary policies. The fiscal loosening in place since last year and the ECB’s supportive monetary policy stance have translated into robust consumption growth. However, overall GDP growth is being held back by weaker export growth and sluggish investment, with the latter being weighed down by uncertainty, high levels of corporate debt, and persistent structural bottlenecks.

The weaker economic environment, high corporate debt, and the banking system’s related challenges from high non-performing loans (NPLs) are mutually reinforcing.

As banks continue to struggle with a large stock of NPLs, low profitability, and high operating costs, they are unable to reduce corporate indebtedness and provide adequate lending for investment. Weaker growth in turn, together with low interest rates and low inflation, makes it more difficult for banks to rein in their stock of NPLs and improve profitability.

A concerted policy effort is needed to address the interrelated weaknesses in the banking system, public sector finances, and the macroeconomic outlook.

A credible and realistic fiscal adjustment path — going well beyond achieving a 3 percent headline deficit — is needed to ensure the medium-term sustainability of public finances. This would alleviate significant uncertainty about the direction and scope of future policies and support private sector investment plans. Structural reforms to promote growth and competitiveness, and efforts to improve banks’ governance, would boost this positive dynamic. Lower uncertainty and improved growth prospects would in turn help support a strengthening of bank balance sheets, reduce potential fiscal costs of supporting banks, and facilitate the required fiscal consolidation.

Media Relations

E-mail: media@imf.org

Phone: 202-623-7100

page source http://www.imf.org/