NEWS Release - The Global Trade Slowdown and Its Implications for Emerging Asia - Governor Jerome H. Powell - At "CPBS 2016 Pacific Basin Research Conference," sponsored by the Center for Pacific Basin Studies at the Federal Reserve Bank of San Francisco, - San Francisco, California - November 18, 2016

It is a pleasure for me to return to the Center for Pacific Basin Studies here at the San Francisco Fed. The global economy is at a critical juncture today. According to the International Monetary Fund's latest World Economic Outlook, global gross domestic product (GDP) is set to grow at only 3.1 percent this year, the lowest rate of growth since the Global Financial Crisis.

Investment and productivity remain subdued, despite extremely low and even negative interest rates in many economies.1 One key aspect of global weakness that is of particular relevance to emerging Asian economies is the sharp slowdown in global trade. This slowdown represents a notable departure from the "normal" times of the past few decades, and is the subject of my remarks today.2

More specifically, I will discuss four topics. First, I will review the main features of the global trade slowdown and summarize the evidence on its potential causes. Second, I will examine the special role that structural changes in China appear to be playing in the trade slowdown. Third, I will turn to the implications of this slowdown for economic growth in the region. And, finally, I will offer some views on how Asian economies can respond to the slowdown by rethinking their "export-led growth" paradigm.

Documenting the Global Trade Slowdown and Its Likely Causes

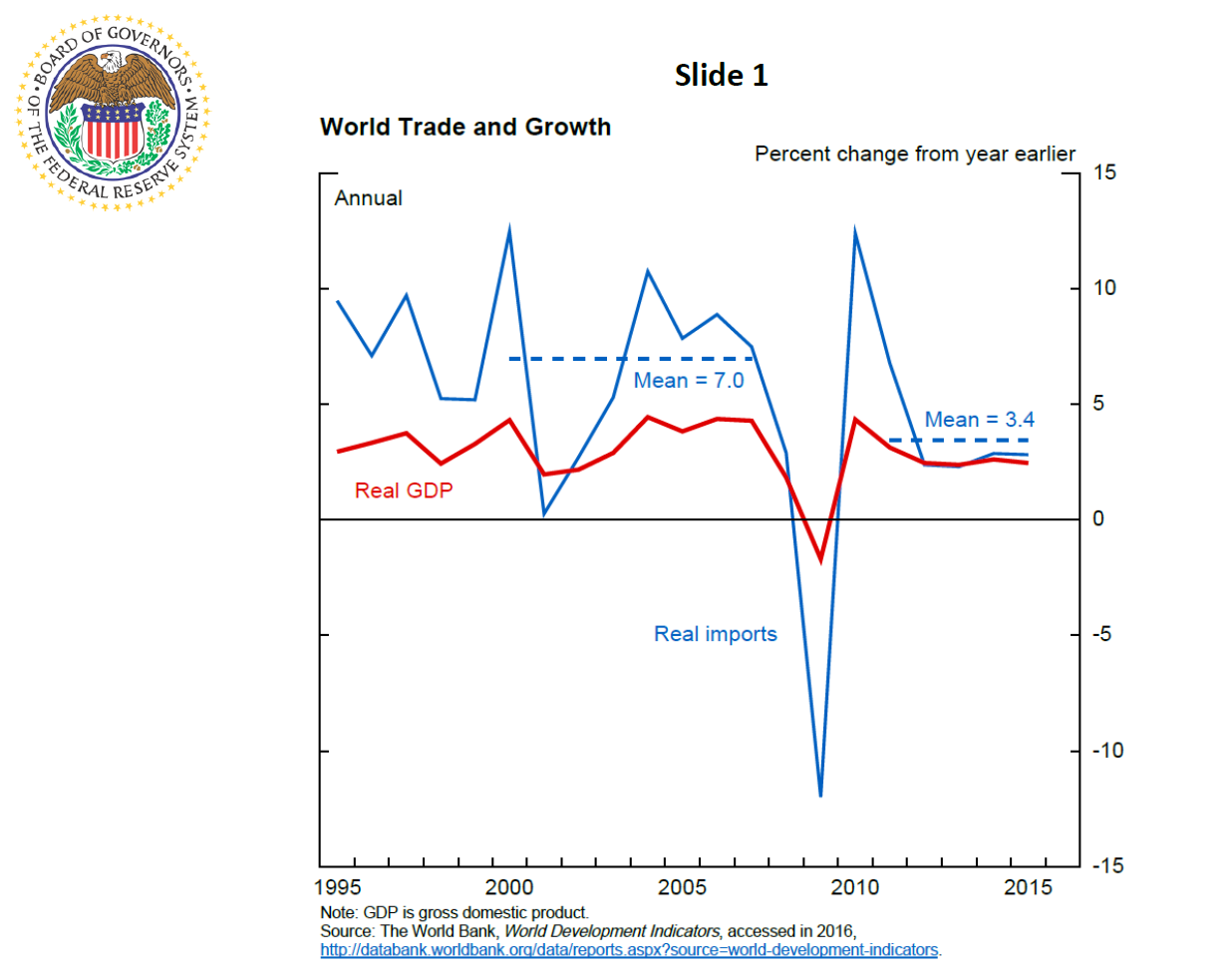

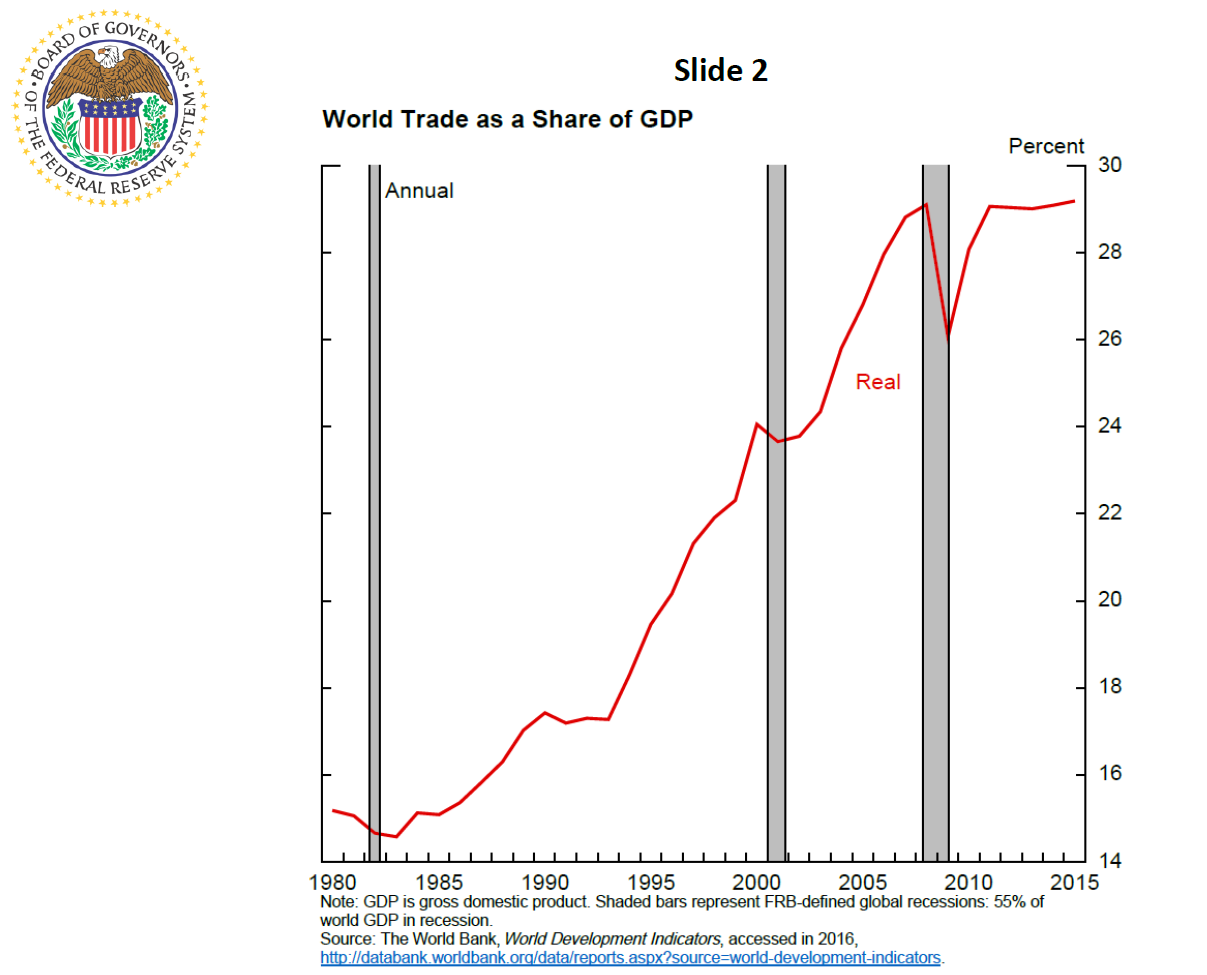

To set the scene, I will review the main features of the recent global trade slowdown. As you can see on the first slide, growth in world trade rebounded after the Great Recession but has slowed substantially since 2011. On a real inflation-adjusted basis, world imports have grown at an average annual rate of less than 3-1/2 percent since 2011, about half the 7 percent pace seen in the eight years prior to the Global Financial Crisis.3 As illustrated in the next slide, trade is no longer outpacing GDP growth. The share of real world imports in world GDP has been flat at just under 30 percent since 2011 after nearly doubling between 1985 and 2007.4 This sustained slowing of real trade relative to GDP is quite unusual: Since 1870, trade has generally grown faster than production, outside of wartime and recessionary periods.

{kind=link}

{kind=link}

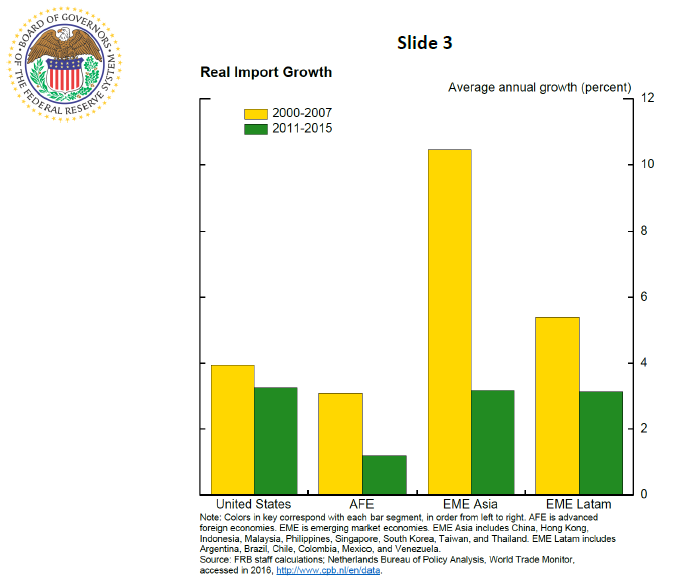

Trade has been sluggish almost everywhere. Real trade growth has been lower over the 2011-15 period compared with the 2000-07 period for every G-20 country outside of Japan, where trade growth was constant. The third slide shows that the fall in real import growth in emerging Asia has been particularly pronounced from over 10 percent in the first period to just about 3 percent in the second. But import growth has declined in Latin America and the advanced economies as well.

{kind=link}

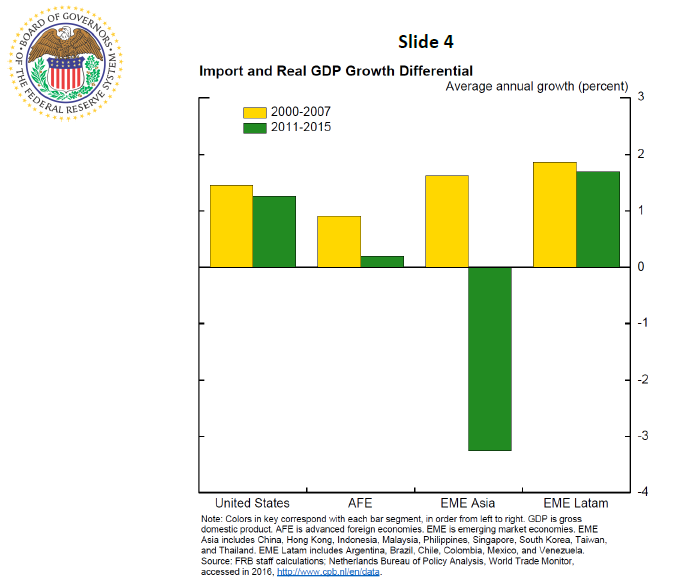

The next slide shows the differential between real import growth and real GDP growth for the same two periods. For emerging Asia, the differential went from positive to substantially negative, indicating that real import growth slowed to well below real GDP growth. In advanced foreign economies, the differential was just about zero in the more recent period, indicating that real import growth barely kept pace with GDP growth. Trade relative to GDP has held up better, though, in the United States and Latin America.

{kind=link}

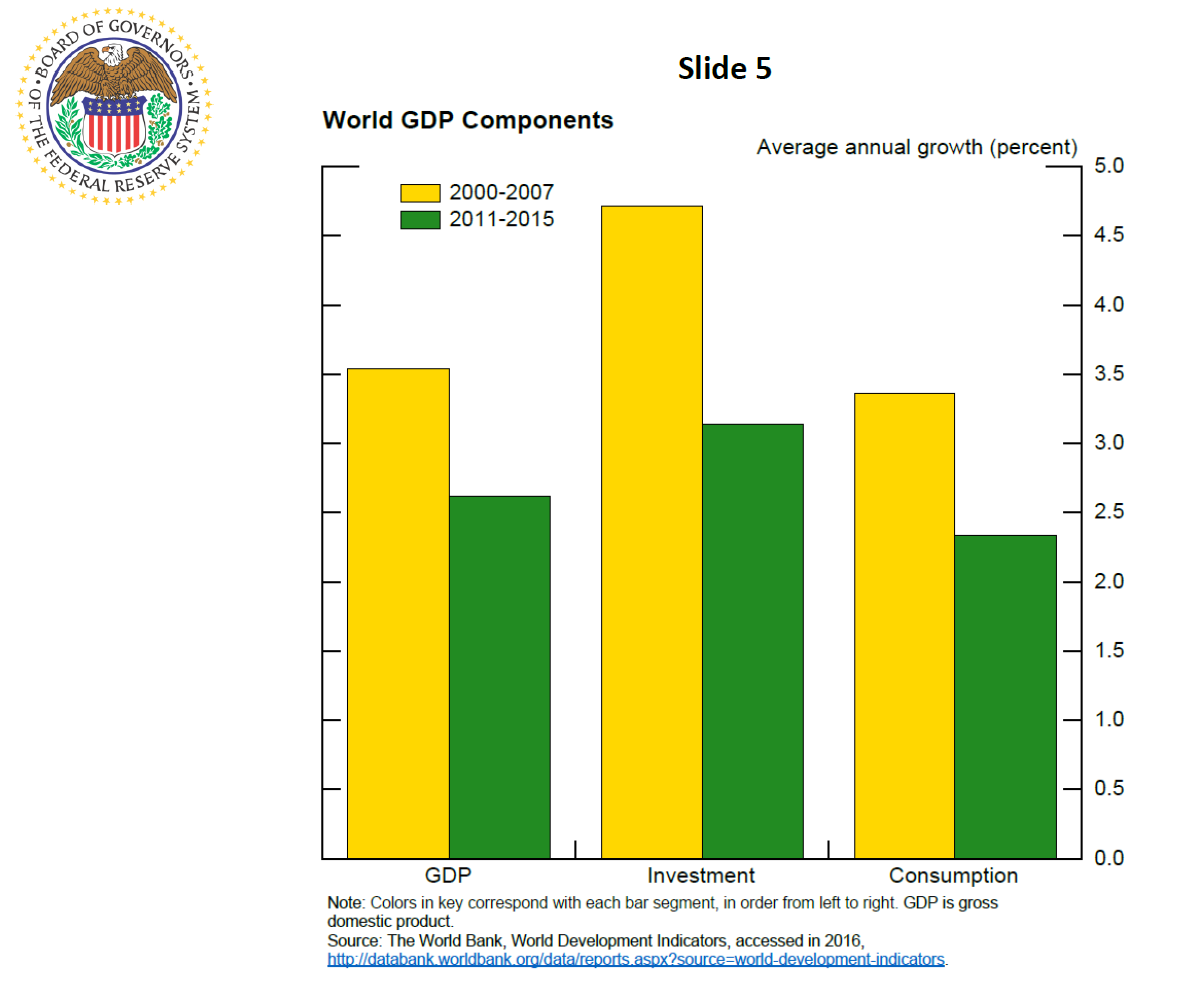

Is the trade slowdown just another manifestation of slow growth, or is it an independent concern? That depends on the reasons for the slowdown. Weak global growth is surely part of the explanation, as emphasized by several recent empirical studies, including a special chapter on the topic in the latest IMF World Economic Outlook.5 As can be seen in slide 5, global GDP growth has fallen from an average of 3.5 percent before the Global Financial Crisis to about 2.5 percent since its end.

{kind=link}

But weak global growth alone does not explain why trade has slowed to about the same pace as GDP after growing faster than GDP for decades. Part of the reason could be that the particular expenditure categories in which international trade flows are concentrated have become especially weak. A stark case in point is the Global Financial Crisis, when plummeting demand for investment and durable goods--two highly traded expenditure categories--contributed to the sharp 4 percentage point fall in the ratio of world trade to GDP. The special weakness in some components of demand has persisted beyond the crisis and could also explain some of the recent sluggishness in trade relative to GDP. In particular, as you can see from the middle two bars of slide 5, the slowdown in world investment growth--from about 4.5 percent growth before the Global Financial Crisis to only about 3 percent growth since 2011--has been more pronounced than the slowdown in world GDP growth or in world consumption. But the differences are not huge, suggesting that this explanation can go only so far.

Indeed, research suggests that other factors are also important in accounting for the slowdown in world trade.6 One such factor is the deceleration in the pace of trade liberalization policies. From the early 1990s through the mid-2000s, trade barriers were coming down rapidly, including the signing of the North American Free Trade Agreement in 1994, the 2001 entry of China into the World Trade Organization, and the 2005 expiration of the multifibre agreement restricting textile imports to the United States and European Union. These changes resulted in the most rapid increases in the trade-to-GDP ratio since 1870. As the pace of trade liberalization has slowed in recent years, perhaps reflecting limits to further gains from trade agreements, it is only natural that the trade-to-GDP ratio should flatten out as well.

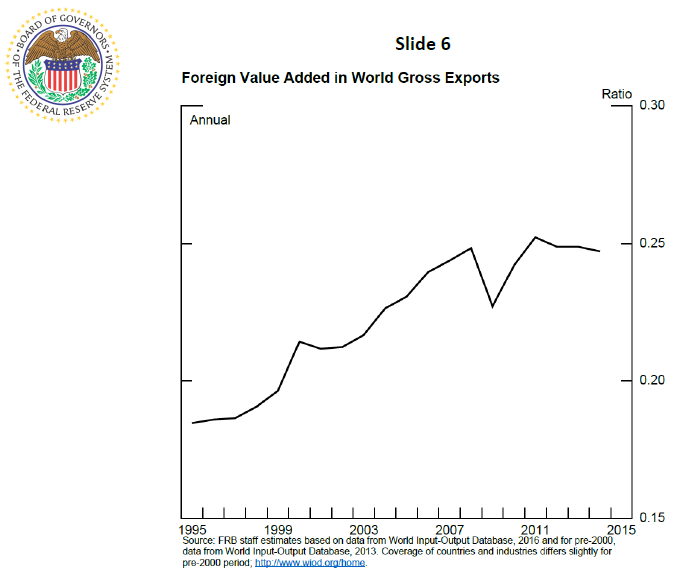

Another related factor is the maturation of global value chains. Increased fragmentation of production across international borders--a natural outgrowth of the gains from specialization--meant more trade for any given value of final production, thus adding to the major expansion in gross trade flows in the 1990s and 2000s. As shown in the next slide, global value chain participation, as measured by the share of foreign value added in world exports, increased substantially during this period. It is quite plausible that the process of increased fragmentation of production across borders is subject to "diminishing returns" and has its natural limits. Consistent with this notion, the trend toward greater product fragmentation has slowed in recent years.

{kind=link}

Finally, of course, China looms large in any discussion of the global trade slowdown. Not only is China's trade being affected by all of the factors just discussed, but on-going structural changes within the Chinese economy, including rebalancing toward domestic demand, are exerting an independent effect on world trade flows. So, let's look next at China in more detail.7

China

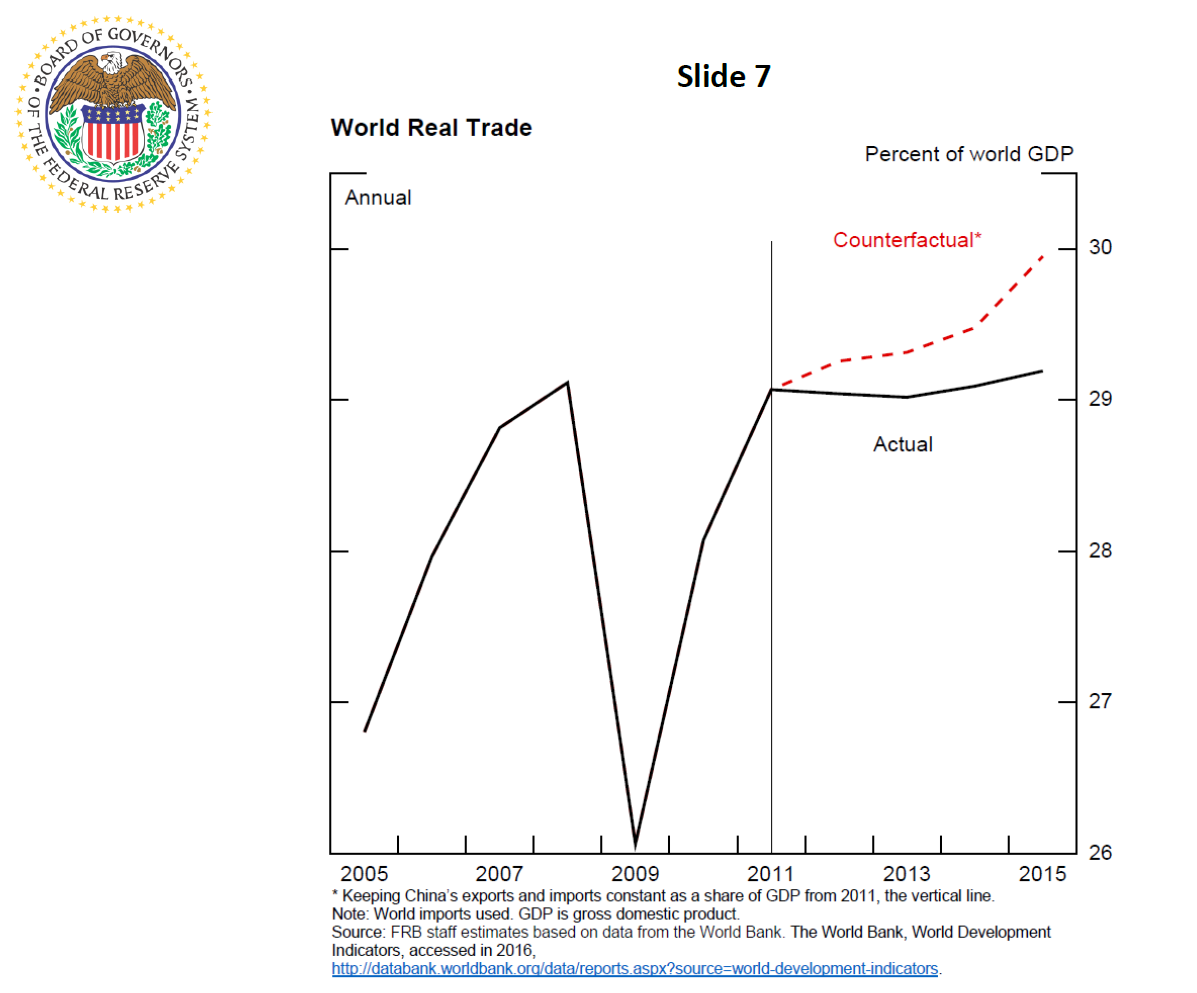

After years of rapid export-led growth, China is now among the world's leaders in both exports and imports. China's exports now account for 14 percent of the world's total, compared with only 4 percent 15 years ago. At the same time, China's industrialization and export model has greatly increased its own demand for imports of raw materials, intermediate inputs, and parts and components. In recent years, however, growth in both Chinese imports and Chinese exports has slowed markedly. These developments have had a significant effect on global trade. One simple way to measure that effect is to consider what would have happened if China's trade had not decelerated. As shown in slide 7, under a counterfactual in which China's trade growth had not slowed relative to its GDP since 2011, global trade would still be growing as a share of GDP.8

{kind=link}

20th Street and Constitution Avenue N.W.

Washington, D.C. 20551

page source https://www.federalreserve.gov/